Tech Explained: Here’s a simplified explanation of the latest technology update around Tech Explained: Big Tech Is Spending $720 Billion on AI in 2026, and This One Stock Gets Paid on Every Dollar in Simple Termsand what it means for users..

Over the last few weeks, technology companies reported their results for calendar 2025 and issued financial guidance for this year. Meanwhile, on Wall Street, the main theme that investors have been obsessing over is how much money big tech will be spending on artificial intelligence (AI) infrastructure this year.

The big five hyperscalers guided for 2026 capital expenditure (capex) budgets as follows:

- Meta Platforms: $115 billion to $135 billion

- Amazon: $200 billion

- Microsoft: $150 billion (run rate)

- Alphabet: $175 billion to $185 billion

- Oracle: $50 billion

At the high end of those guidance ranges, the hyperscalers are expected to spend a whopping $720 billion on AI capex this year. With that in mind, one could expect the biggest beneficiaries to be AI chip designers such as Nvidia, Advanced Micro Devices, and Broadcom.

However, the company I see benefiting the most from rising AI infrastructure spend is a quieter leader: Taiwan Semiconductor Manufacturing (TSM +1.93%).

Image source: Taiwan Semiconductor Manufacturing.

Taiwan Semiconductor’s growth is astronomical, and it’s not slowing down anytime soon

Taiwan Semiconductor is the largest chip manufacturer in the world by revenue. With an estimated 71% share of the third-party chip foundry market, TSMC has become the foundry partner of choice for designers of GPUs, AI accelerators, and custom application-specific integrated circuits (ASICs).

The company’s competitive edge rests on its unmatched ability to manufacture the most cutting-edge, powerful, and transistor-dense chips without flaws and at scale. So as the hyperscalers keep doubling down on their AI data center buildouts, TSMC is a key manufacturer of the processor chips those facilities need.

In essence, this means that when companies like Nvidia, AMD, and Broadcom publish strong results and issue encouraging guidance, Taiwan Semi is in the background, profiting from all of their successes.

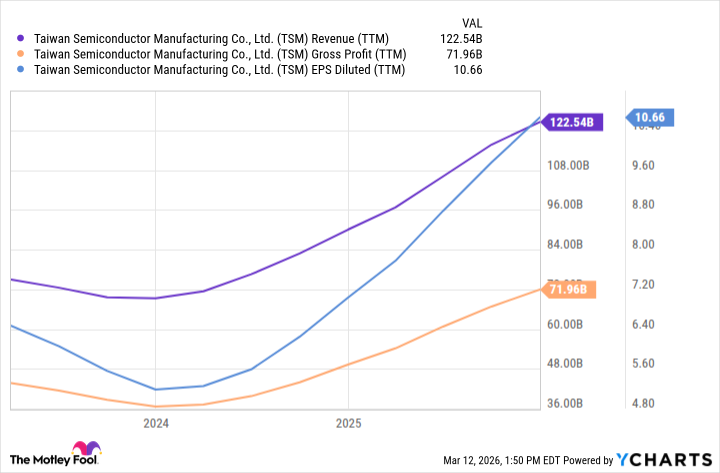

To get a sense of how instrumental Taiwan Semi’s role is to the chip narrative, take a look at the company’s financial profile over the last few years.

TSM Revenue (TTM) data by YCharts.

Throughout the AI revolution, the company’s revenue, gross profit, and earnings have surged significantly. Not only are TSMC’s services in demand, but the company also commands meaningful pricing power.

Big tech is gearing up for another year of monster spending, and given that Taiwan Semi exists as something of a tollbooth along the AI chip value chain, it will book incrementally higher sales and profits along the way.

Is Taiwan Semi stock a buy right now?

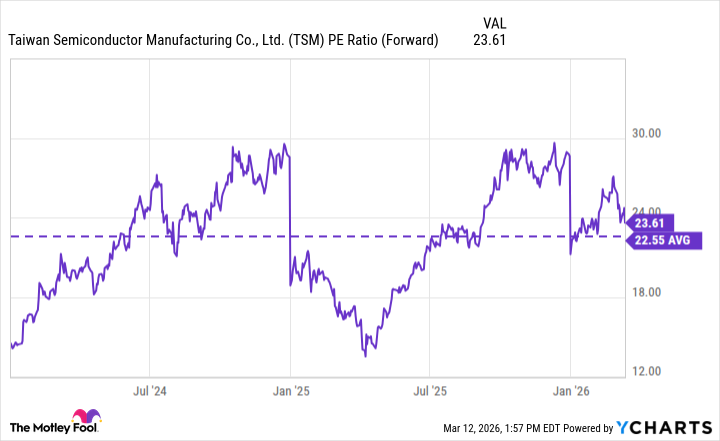

There are several ways for investors to weigh the value of a stock. For a hypergrowth company like Taiwan Semi, I prefer to look at the forward price-to-earnings (P/E) ratio. That’s because this metric measures its current valuation against what Wall Street expects it to earn.

TSM PE Ratio (Forward) data by YCharts.

At the moment, TSMC’s forward P/E multiple is 23.6 — barely above its three-year average and well below its recent peak of about 30. I think the discount to its former premium boils down to one specific detail: Some investors are unsure that the hyperscalers will actually sustain their capex ambitions.

In other words, the pace at which infrastructure costs are rising is outpacing growth rates in operating and free cash flows. Against this backdrop, if the hyperscalers suddenly decide to cut back on their capital spending, TSMC’s backlog could be affected.

While I understand these concerns in theory, there have been no signs over the last three years that the big tech players have any plans to slow their infrastructure buildouts. In my view, Taiwan Semi’s discounted valuation is based more on a narrative than on observable facts.

Spending on the overall AI infrastructure buildout could very well eclipse trillions of dollars through the remainder of the decade. Given TSMC’s unique role as a manufacturer of both high-end general-purpose chips and custom silicon solutions, I do not anticipate the company’s growth trajectory getting bumpy anytime soon.

For this reason, I see TSMC as a no-brainer stock to buy and hold over the next several years.

Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, Oracle, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.